Morning Report: The Fed remains divided on rate cuts

Vital Statistics:

Stocks are flattish this morning despite news that Trump intends to raise tariffs on Brazil. Bonds and MBS are up.

The US Treasury auctioned off $39B of 10 year notes yesterday which was met with strong demand. The yield of 3.62% was lower than the market ahead of the auction and the 2.61 bid / cover ratio indicates a good reception. This put a spring in the step of the bond market and yields went out yesterday on their lows.

It seems like the market is beginning to tune out the tariff noise.

The FOMC Minutes were released yesterday. The Fed's view is pretty clear: they believe the labor market is at or near full employment, inflation remains above their target, and tariff uncertainty is the most important factor driving policy.

In considering the outlook for monetary policy, participants generally agreed that, with economic growth and the labor market still solid and current monetary policy moderately or modestly restrictive, the Committee was well positioned to wait for more clarity on the outlook for inflation and economic activity.

Participants noted that monetary policy would be informed by a wide range of incoming data, the economic outlook, and the balance of risks. Most participants assessed that some reduction in the target range for the federal funds rate this year would likely be appropriate, noting that upward pressure on inflation from tariffs may be temporary or modest, that medium- and longer-term inflation expectations had remained well anchored, or that some weakening of economic activity and labor market conditions could occur.

A couple of participants noted that, if the data evolve in line with their expectations, they would be open to considering a reduction in the target range for the policy rate as soon as at the next meeting. Some participants saw the most likely appropriate path of monetary policy as involving no reductions in the target range for the federal funds rate this year, noting that recent inflation readings had continued to exceed the Committee's 2 percent goal, that upside risks to inflation remained meaningful in light of factors such as elevated short-term inflation expectations of businesses and households, or that they expected that the economy would remain resilient. Several participants commented that the current target range for the federal funds rate may not be far above its neutral level.

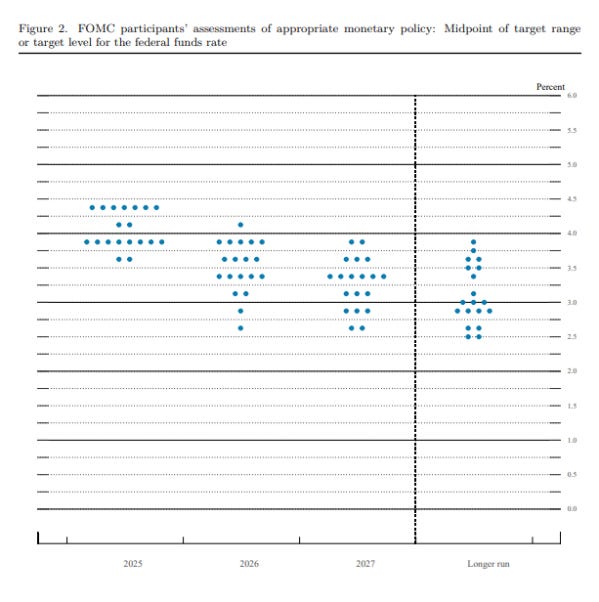

A lot to unpack in that last paragraph. So we have "a couple" of participants that are open to easing rates at the July meeting. We also have "some" participants who think there should be no cuts this year, and "several" (could be the same people who think there should be no cuts) who think the Fed Funds rate is already close to r-star, which means they think the long term Fed Funds rate should be in the 4% range.

Indeed, there are a few dots in the far left column that are in the 3.5% - 4.0% range. Overall, the consensus still seems to be that r-star is in the low 3% range, probably between 3.0% and 3.25%.

So 7 out of 19 voters think there should be no rate cuts this year, while the biggest plurality think 2 cuts would be appropriate, which is what the Fed Funds futures are predicting. A July cut is a long shot, especially since the new tariff deadline is August 1.

IMO, the labor market isn't as strong as the statistics indicate - the low unemployment rate is being driven by people exiting the labor force. Job openings may be high, but how many of these are simply ghost jobs that don't really exist? Finally, the gig economy makes a lot of people ineligible for unemployment benefits, which means low initial jobless claims aren't really the same as they were a decade ago.

AI is already replacing a lot of jobs, which will depress consumer spending. The Fed is probably closer to causing a recession than it thinks.

Rate lock volume increased 2% in June, according to Optimal Blue. Non-QM locks are accounting for an increasing percentage of total volume, rising to 7.4% in June. “As market conditions evolve and affordability challenges persist, non-QM lending offers a path for qualifying creditworthy borrowers who may not meet qualified mortgage guidelines,” said Mike Vough, head of corporate strategy at Optimal Blue. “The steady rise in this category reflects the industry's growing focus on flexibility and meeting borrowers where they are.”