The inflationary and deflationary forces emanating out of Asia.

As expected, the Fed hiked the Fed Funds rate by 25 basis points at the July FOMC meeting. Investors hoping to hear an “all-clear” signal from the Fed were disappointed however. The language in the FOMC statement made no mention of any concerns over the state of the economy or anything that could be interpreted as viewing the balance of risks between growth and inflation as equally weighted. In the press conference, the business press asked a lot of questions regarding when the Fed will consider its work to be done, and Jerome Powell didn’t take the bait.

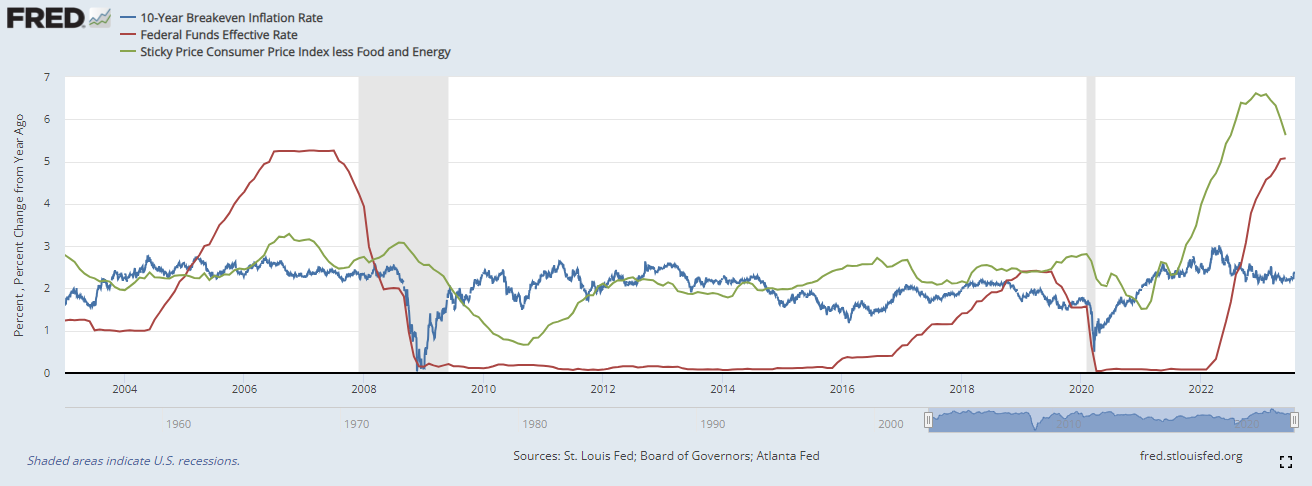

Jerome Powell was asked about how restrictive the Fed is currently, and he discussed the Fed Funds rate versus inflationary expectations. Inflationary expectations are a somewhat squishy subject, but you can kind of determine them by looking at the breakeven rates on the 10 year Treasury Inflation Protected Securities (TIPS). These are Treasuries that pay a low rate of interest, but the principal increases in value over time based on the Consumer Price Index.

Since TIPS and normal Treasuries have the same credit risk (i.e. none) you can compare the price between the TIPS security and the corresponding 10 year and calculate the inflation rate that the TIPS security is pricing in. This is called the breakeven inflation rate, and it means that if inflation comes in lower, you will be better off in the plain old Treasury and if inflation comes in higher, you will be better off with the TIPS bond. The breakeven inflation rate can be interpreted as the market’s view of inflationary expectations and it is much more robust than looking at sentiment indicators like the University of Michigan Consumer Sentiment Survey.

Below is a chart of the Fed Funds rate versus inflationary expectations as measured by the breakeven rate on TIPS. I have included the sticky CPI as well, which is the Consumer Price Index less food and energy.

The surprising thing is how stable inflationary expectations have been during this period of elevated inflation. The breakeven rate on the TIPS increased by about 50 basis points in mid-2022, however it has come back close to the Fed’s 2% target. The market thinks the Fed has control over inflation and will bring it down to 2% in relatively short order. Unfortunately, TIPS were only introduced in 2003, so this is the first time we have seen how they perform in an inflationary environment.

We saw a big increase in the yield in the Japanese Government Bond last week after the Bank of Japan tweaked the language in a statement on monetary policy. The Bank of Japan has employed an unusual policy of direct yield targeting. Unlike the Fed’s policy of quantitative easing, where the Fed would buy Treasuries to influence long term rates, the Bank of Japan was imposing a ceiling on long term rates.

Japan was somewhat of a pioneer in government meddling in markets. After the Nikkei 225 crashed in 1989, the Japanese government would try to maintain a floor on stock prices using what was called a “price-keeping” operation. The Japanese economy was always a bit of a convoy operation, with companies holding large stakes in each other. This was especially true with the banks. It helped grease the skids for industrial policy and it also made corporate governance pretty much meaningless. Everything was decided by consensus with the government.

The problem for the Japanese banks was that they marked their holdings of these companies at cost. This was not a problem when the stock market was soaring; it just meant that the book value of the banks was understated. When the stock market reversed, there was a line in the sand around 14,000 on the Nikkei 225. If the stock market was weak in the first session (the Japanese market would break for lunch) you would sometimes see a ferocious rally early in the second session after the Ministry of Finance told the banks and asset managers to tear up their sell tickets for the day. Eventually market forces won out, but stock prices were completely artificial in Japan for decades.

The Bank of Japan did the same thing with the Japanese Government Bond, where yield targeting meant that there was a cap on yields. The Bank of Japan changed the language to imply that the caps were only guidance and not formal caps. This caused yields on the Japanese Government Bond to spike last week, and this will probably be a net drag on bond prices in the global bond markets going forward.

On the other hand, China is experiencing a real estate bust of epic proportions. The country had seen such a spate of overbuilding that prices have become unsustainable. Entire cities have been built on spec. I suspect this sort of thing happens when economies experience several decades of hyper-growth. The US saw several decades of hyper-growth in the early 20th century, culminating in the Crash of 1929. Japan saw that in the 70s and 80s after it completed its rebuild in the aftermath of World War II.

China went through a phase of hyper-growth starting in the 1990s as it joined the global economy. A deep, painful depression seems inevitable for the country, and that will be a massive deflationary pulse going forward. The playbook is generally to devalue the currency and then to try and export a country’s way out of the problem. If China devalues, imports will become much cheaper in the United States, and China will probably run a massive trade surplus. This means additional demand for US Treasuries and mortgage backed securities.

It might be this effect that is driving the surprisingly low inflation forecast we are seeing in the TIPS market.