The Weekly Tearsheet: A volatile week for bonds

Last week was pretty volatile for the bond market, however rates didn’t move all that much when all was said and done. Last week we had the Fed meeting, where the Federal Open Market Committee maintained interest rates at current levels and did not signal any imminent rate cut discussions. That said, bond bulls pushed down yields on the 10 year down to 3.84% on Thursday. Friday’s jobs report came in much stronger than expected, and that pushed bond yields back up above 4%, which was pretty much where the market began the week.

The action in the Fed Funds futures was pretty dramatic, with the market now decisively predicting no rate cut at the March meeting with a 85% probability. It was roughly a 50-50 chance a week ago, A month ago, the markets saw a 66% chance of a rate cut.

Powell’s statements weren’t really the impetus for the big back up in yields - it was the strong jobs report on Friday, which showed 353,000 jobs were created in January. The interesting thing is that if you look at the actual number of people employed, there were 31,000 jobs lost in January. The table below comes from the jobs report, and the yellow highlighted numbers show the number of people employed.

At the end of December, there were 161,183,000 people working in the United States. At the end of January, there were 161,152,000 people working, which is a decline of 31,000 jobs. So why did BLS report that there were 353,000 jobs created? Demographic and seasonal adjustments. In other words, there were not 353,000 jobs created in January - the 353,000 jobs were created by statistical adjustments.

Take a look at the January 2023 number. It looks like there were 1 million jobs created in 2023 if you look at actual people employed. BLS is claiming that just over 3 million jobs were created in 2023. So 2 out of 3 jobs created in 2023 were due to modeling issues, not people actually getting paychecks.

The Biden Administration is working hard to sell its economic performance, and perhaps part of the reason why consumer confidence remains soft is because of many of these numbers are statistical abstracts that aren’t really reflecting the facts on the ground. Big Tech is seeing layoffs as the world adjusts from a prolonged period of 0% interest rates and free money. Media companies are also letting people go and certainly the mortgage business is struggling.

It also explains why the ADP Employment Report showed only 107,000 jobs were created. ADP is a huge payroll processor, so it has the pulse on what employers are actually doing. As I have said before, there seems to be a mismatch between the numbers coming out of official government agencies and those coming out of non-government entities like ADP, ISM, the NFIB and the Conference Board.

Jerome Powell got on 60 Minutes on Sunday night and said the Fed isn’t going to wait for inflation to get to 2% before starting to cut rates. The Fed wants to be on sustainable path for inflation to get to 2% before cutting. That said, he did also say that it is unlikely that voting members will reach that consensus by the March meeting, which has global markets pulling back rate cut bets.

Regional bank New York Community Bank, which bought Signature Bank during the regional bank crisis tumbled 42% last week after reporting dismal results for the 4th quarter. The bank lost 36 cents a share while the Street was looking for a profit of 27 cents. With the acquisition of Signature and Flagstar in 2022, NYCB now has over $100 billion in assets, which means that it has stricter capital requirements. It cut its dividend to shore up its capital base, and reported that it is starting to see problems in commercial real estate and property loans. Charge-offs surged due to a bad office property loan and a co-op loan.

If we are starting to see issues in the banking system, the Fed will cut rates sooner rather than later. As of now, the soft landing narrative is dominant, but consumers have been on borrowed time and the excess savings from the pandemic are almost gone.

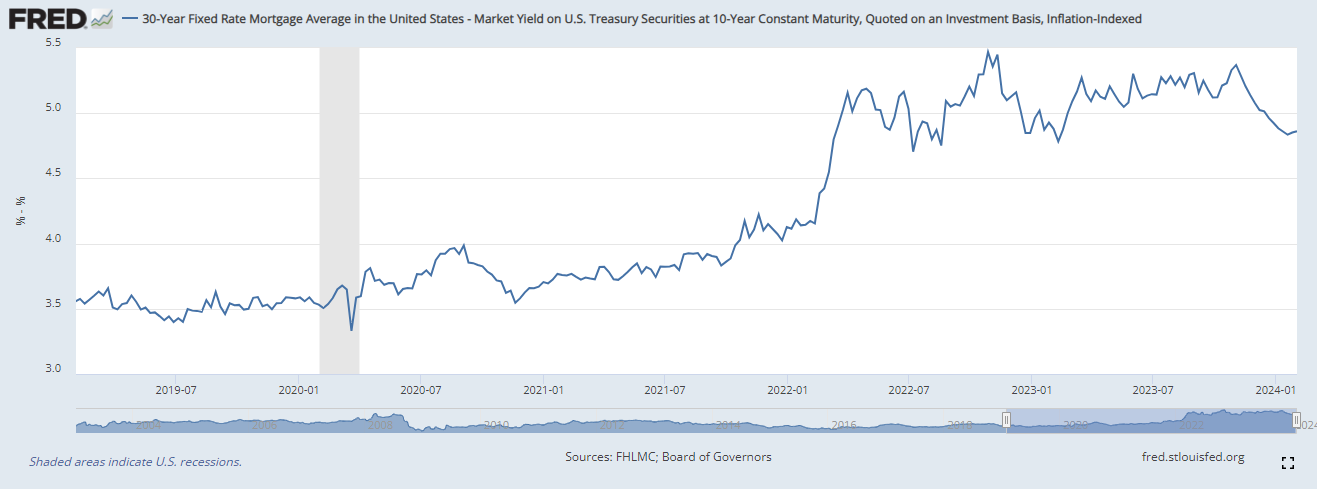

We are starting to see mortgage rates decrease relative to the 10 year as MBS spreads are beginning to decline. The chart below shows the 30 year fixed rate mortgage minus the yield on the 10 year bond. Prior to 2020, the difference between the two was about 3.6%. Today it is above 4.8%. If we get back to normal MBS spreads we could see a 1.2% decline in mortgage rates, which would put the typical 30 year fixed rate in the low 5% range. At that point, we should see less of a rate lock-in effect and maybe some debt consolidation cash out refinances. The Mortgage Bankers Association has been taking up estimates for 2024 and they are beginning to forecast an end to the nuclear winter that has beset the industry for the past two years.