Things are looking up for the mortgage industry, but cracks appear in credit

The past couple of weeks have seen a bunch of ostensibly bad news for the bond market fail to move the march towards lower rates. It is somewhat perplexing to think that the Fed would start easing aggressively after executing one of the most drastic tightening policies in history. The 525 basis points in rate hikes is close to what Paul Volcker did in the early 1980s to vanquish 1970s inflation. Jerome Powell has stressed that the biggest mistake the Fed could make is to repeat the errors of the 1970s - tightening and then easing too quickly. Despite the data and the Fed-speak markets are pricing in a pretty aggressive easing cycle for 2024.

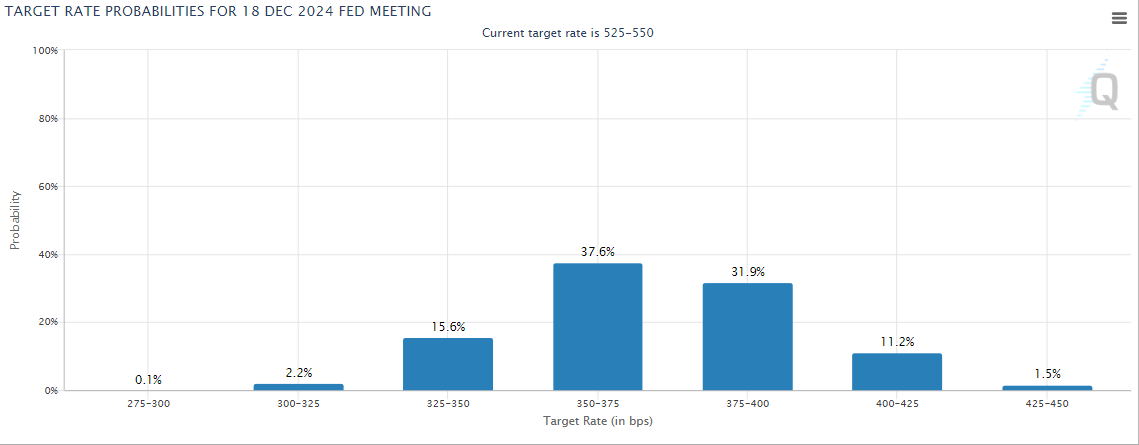

The December 2024 Fed Funds futures now see 175 basis points in rate cuts during 2024:

Interestingly, the data and the body language out of the Fed don’t indicate that this should happen. Perhaps, as I alluded to in my prior column, the Fed is so concerned about a potential Donald Trump victory that they will goose the economy in order to support Biden and then deal with any economic fallout later.

The jobs report on came in stronger than expected, although the trend in payrolls has been on the way down, and over the past 11 months, we have seen payroll numbers for Jan-Nov revised downward by a total of 329,000 jobs or about 1.5 months’ worth of job growth.

The FOMC minutes gave no indication the Fed is worried about an economic slowdown. That said, the Fed does expect to start moving down the Fed Funds rate going into the end of the year. There is still a pretty big disconnect between the market expectations and the Fed however.

The Consumer Price Index came in hotter than expected, although shelter remains the biggest contributor to the index. The Producer Price Index came in lower than expected, which is good news for inflation and rate cut advocates. The PPI generally leads the CPI, which points to lower inflation going forward.

Earnings season is upon us, and the big banks have already reported. Citigroup reported lower-than-expected earnings along with declining revenue growth. Citi had a FDIC assessment that negatively impacted earnings. On the earnings conference call, CEO Jane Fraser sounded somewhat downbeat on the economy:

The global macro backdrop remains a story of de-synchronization. In the U.S., recent data implies a soft landing, but history would suggest otherwise. And we are seeing cracks in the lower FICO consumers…September is always a busy month seeing clients, and I am struck how consistently CEOs are less optimistic about 2024 than a few months ago. The shift in the rates question from how high to how long has catalyzed more client activity, however. Corporates have stopped waiting for rates to come down and are beginning to access the debt capital markets around the globe.

The part about corporates accessing the debt capital markets could mean that corporate borrowers are taking down debt ahead of a potential credit crunch. Citi’s credit losses were up 22% on a quarterly basis and a whopping 66% on an annual basis. Citi also announced plans to cut about 20,000 jobs.

JP Morgan also had a FDIC assessment which impacted earnings, however revenues rose 15% year-over-year due to the First Republic transaction. Like Citi, JP Morgan saw increases in credit losses. Provisions for credit losses rose 100% on a quarterly basis and 22% on an annual basis. In the press release, Jamie Dimon had this to say about the state of the economy:

The U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing. It is important to note that the economy is being fueled by large amounts of government deficit spending and past stimulus…There is also an ongoing need for increased spending due to the green economy, the restructuring of global supply chains, higher military spending and rising healthcare costs. This may lead inflation to be stickier and rates to be higher than markets expect. On top of this, there are a number of downside risks to watch. Quantitative tightening is draining over $900 billion of liquidity from the system annually, and we have never seen a full cycle of tightening. And the ongoing wars in Ukraine and the Middle East have the potential to disrupt energy and food markets, migration, and military and economic relationships, in addition to their dreadful human cost. These significant and somewhat unprecedented forces cause us to remain cautious. While we hope for the best, the past year demonstrated why we must be prepared for any environment.

On the earnings conference call, the company said it was seeing some credit issues in commercial real estate, particularly office however losses were about as expected. It will be interesting to see if delinquencies continue to rise.

For mortgage bankers, the move lower in rates is definitely good news, and the MBA has taken up its forecast for 2024 origination to about $2 trillion, which means a better 2024 than 2023. One of the things that saved mortgage bankers in 2023 was mortgage servicing, and if delinquencies are rising while rates are falling, we should see a sizeable compression in MSR multiples. This will certainly affect MSR-centric companies like Mr. Cooper and PennyMac. With tightening MBS spreads and falling interest rates the agency mortgage REITs like AGNC Investment could be attractive. Bill Gross has been recommending the mortgage REIT space. If the yield curve un-inverts as the Fed Funds rate falls, we should see a much less dramatic move in the 10-year, which means prepay speeds may not increase all that much, while tightening MBS spreads make MBS portfolios worth more.

In the real estate space, it is probably too early too look at the originators, but the mREITs do look interesting.