Week In Review: More hawkish Fed-Speak.

Last week, the markets priced in another quarter point increase in the Fed Funds rate. The probability of a June 25 basis point hike increased from 18% to 71%. Hawkish comments at the beginning of the week laid the foundation, and then the Fed minutes along with a hot PCE print sealed the deal.

It started with St. Louis Fed President James Bullard suggesting that another 50 basis points of rate hikes might still be needed to get inflation under control. “I think we're going to have to grind higher with the policy rate in order to put enough downward pressure on inflation….I'm thinking two more moves this year, not exactly sure where those would be. But I've often advocated sooner rather than later….As long as the labor market is so good it is a great time to get this problem behind us and not replay the 1970s.”

San Francisco Fed President Mary Daly was more circumspect, emphasizing the data "We have to be extremely data-dependent, and that's why, even three weeks in advance of the meeting, our next meeting, it's still a lot of time to collect information before we make a decision about what to do in June or what to do for the rest of the year."

The FOMC minutes were released on Wednesday, and the big takeaways were that the regional bank situations seems to be over, and the Fed thinks the risks to the economy are on the side of inflation, not recession. Finally, we got the PCE Price Index, which is the Fed’s preferred measure of inflation. It showed that inflation ticked up mildly in April, although the trend over the past year is decidedly down. We also saw an uptick in inflationary expectations in the University of Michigan Consumer Sentiment Survey.

Bullard’s comments about the labor market being so good is important, and I think it reveals a bit about the Fed’s mindset regarding historic interest rates. It is easy to forget that 0% interest rates had never existed before in history. This isn’t normal, and I think the Fed really, really wants to get things back to charted waters.

It wasn’t long ago that you could buy German Bunds at negative interest rates. Most short term bonds are simply a “pay now for money in the future model.” Treasury bills are sold at a discount to par. Investors pay 98 cents to get a dollar 3 months from now. When rates were negative, you would pay a dollar to get 98 cents 3 months from now. Why would anyone do that? Because of the incentives from unorthodox monetary policy by central banks to stimulate an economy in the aftermath of a deflationary bust. This was engineered, and it is truly unprecedented. I think the closest we ever got in the past to the concept of negative interest rates was when people would pay someone to guard their gold.

Late on Sunday, it looked like a compromise on the debt ceiling was near, which pushed rates down on Tuesday. The possibility of a real default was close to zero, although the business press worked hard to condemn Kevin McCarthy for using his negotiating leverage to garner spending cuts. Overall, he was largely unsuccessful, although the GOP did get some symbolic wins like clawing back some of the IRS’s enforcement budget and including some limited work requirements to receive food stamps. Overall, the deal will get squawk-back from backbenchers on both sides of the aisle, but its all over but the shouting.

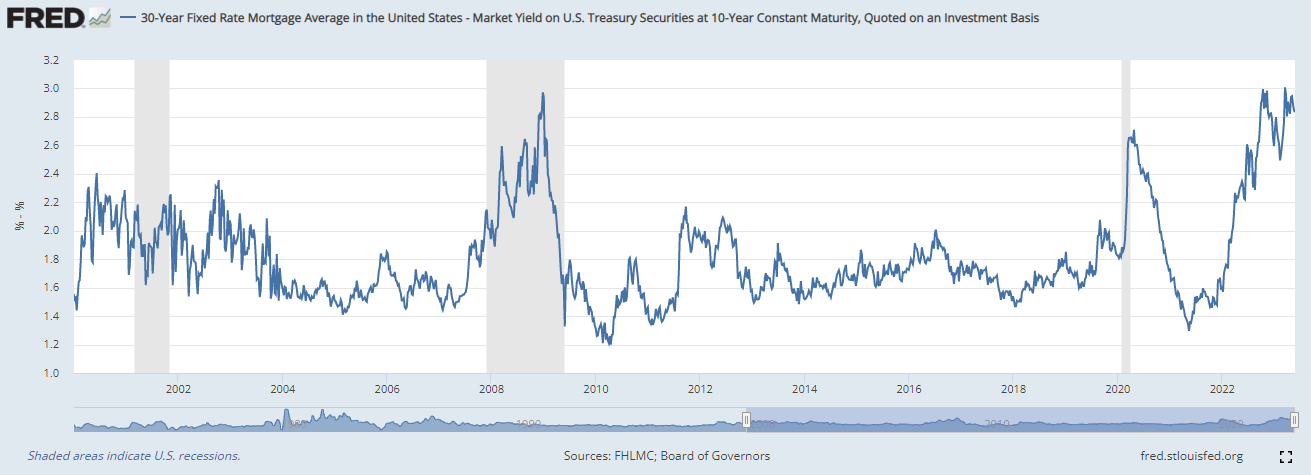

The 10 year and 2 year bond yields fell by 10 basis points on Tuesday, while the 3 month T-bill picked up 14 basis points in yield. While the yield curve remains heavily inverted, some steepening is welcome news for economic bulls. The mortgage industry remains in rate hell as long-term rates remain high and mortgage backed security spreads are pushed out close to the record levels we saw in the 2008 meltdown and late 2022.

The issue with MBS spreads is largely due to uncertainty about the Fed and the fact that regional banks have inventory to go. The FDIC is auctioning off the paper from Silicon Valley Bank and Signature Bank, however other regionals are probably trying to trim positions, and few relative-value investment grade traders are willing to commit capital to the asset class until the smoke clears. Regardless, unless rates begin to fall soon, any second half recovery in mortgage banking will probably be deferred until 2024.

Take a look at the chart above of MBS spreads and compare pre-2008 with post-2008. Does it look like quantitative easing and government purchases of $2.7 trillion in mortgage backed debt made any sort of measurable impact on MBS spreads? Maybe during the pandemic, but the 2008 - 2020 era might have been 20 basis points narrower than pre-QE. Doesn’t seem like much to write home about.

We saw real estate prices start to increase again after a year-long pause. Despite the issues of affordability, demand still remains much higher than supply for houses. Supply is restricted due to limited construction and homeowners choosing to stick with a low mortgage rate over a different home. Homebuilding usually leads the economy out of a recession, however it has been MIA ever since the 2008 downturn. Interestingly, the S&P 500 Homebuilder Index (XHB) has been outperforming the S&P 500 over the past year, so maybe we will finally get to see homebuilding again.