Week in Review: Plotting the Fed Funds Forecast over time

As expected, the Fed delivered a “hawkish pause” at its June meeting last week. The Fed maintained the Fed Funds rate at its current level, but signaled two more rate hikes ahead. Jerome Powell called the July meeting “live” which is being taken as a hint the Fed will hike next month. The Fed Funds futures had been predicting that for a while.

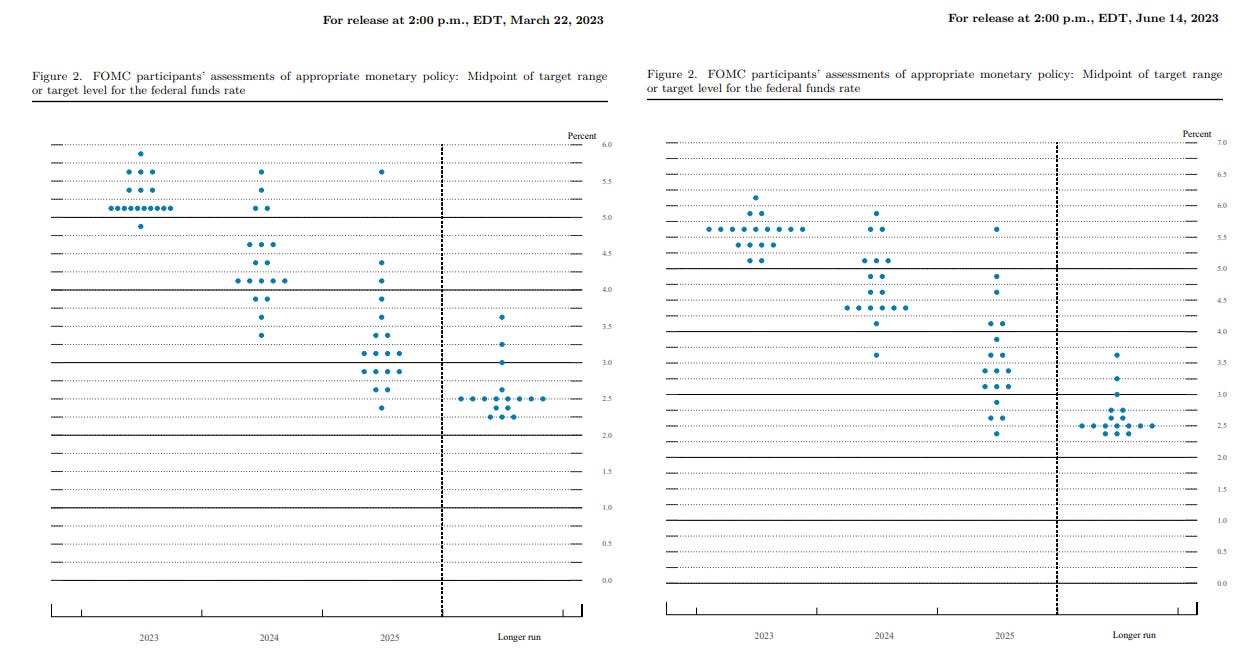

The dot plot comparison is below. The end-of-2023 Fed Funds rate is now looking like 5.5%.

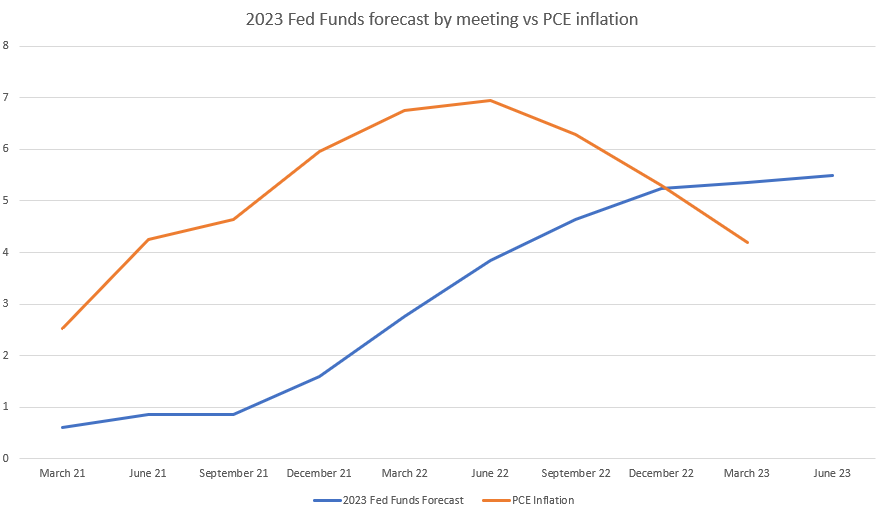

Note that the December Fed Funds futures are not buying this. They assign a relatively small ( <10% ) probability that rates will be 5.5% at the end of December. That is not really a surprise any more; the Fed Funds futures have been overly dovish since this tightening cycle began. In all fairness, the Fed itself has been overly dovish throughout this whole cycle. I was curious so I plotted the Fed’s forecasts for 2023’s Fed Funds rate by meeting starting in March 2021. I also included PCE inflation, which shows how far behind the curve the Fed was.

By mid 2021, inflation was over 4% and the Fed was still predicting that the Fed Funds rate in 2023 would be below 1%. By mid 2022, inflation peaked at 7% and the Fed still thought that the Fed Funds rate would be around 4%. It wasn’t until December of 2022 that real interest rates (i.e. the Fed funds rate minus inflation) turned positive. They had been negative for years. People forget that negative interest rates don’t have much of a history. Central banks haven’t been around all that long in the grand scheme of things, and negative interest rates have never been really tried before.

They say generals always fight the last war, and I think this was going on last year. The most recent memory for the Fed was fighting the deflationary spiral in the aftermath of the residential real estate bubble. Inflation went negative in 2009 and PCE inflation bottomed at -1.5% in 2009. The Fed was mindful of Japan’s experience with its lost decade, and was determined not to make that mistake. Japan didn’t really mess with negative interest rates. The economy never reached escape velocity from 0% interest rates. Rates were pegged to the floor, but in a deflationary environment, 0% interest rates are still positive on an inflation-adjusted basis. The US managed to do that by holding interest rates at 0% and igniting inflation.

Like Japan in the 1990s, the US economy was reeling from a burst residential real estate bubble. These are the Hurricane Katrinas of banking and the economy. Housing is a highly leveraged asset - even a 20% down mortgage, which is considered “conservative” is still 4:1 leverage. And when widely-held and leveraged asset markets fall apart, the shrapnel goes everywhere. People generally have a lot of their net worth tied up in their house. The Great Recession caused people to stop spending, which created a negative feedback loop with hiring. The Fed needed to do something unorthodox, and it did, with QE and inflation targeting. The point was to get credit flowing again and for consumer spending to pick up.

In 2012, the Fed officially introduced an inflation target. This was new. The Fed told the market that it will do what it takes to get inflation up to 2%. The idea was to stop people from saving and to get them spending by telling them they would lose money after inflation if they kept money in the bank. The inflation target was instituted because inflation was too low, not because it was too high. Since the Fed had struggled to lift inflation to 2% and that experience was probably the driver with the Fed’s reluctance to raise interest rates this time around. The Fed had been spoiled by globalization-driven low inflation and the “transitory” language basically assumed that once the COVID-driven supply chain shortages were through, inflation would return to its same old habits.

Of course at this point it is all about sticking the landing for the Fed. UBS was out with a call last week saying their model shows a 80% chance of a recession in the near term. They are making a hard landing call, expecting GDP to contract 1% in the coming months. It will be interesting to see how committed the Fed is to the 2% target or if they will abandon it once the economy enters a recession. If the economy has a hard landing, will they ease if inflation is still running over 2%? The fact that 2024 is an election year is another complicating factor.

We did get some good news on inflation last week. First, the consumer price index showed that inflation continues to moderate. The headline number rose 0.1% month-over-month, and shelter was the biggest component. As I have mentioned in other columns, the residential real estate market peaked in June of 2022, so going forward the real estate portion of inflation will start falling.

The NFIB Small Business Optimism index remains close to historic lows, however it looks like the number of companies raising average selling prices is trending lower. The supply chain / inventory issues still exist, with 20% of respondents saying supply shortages have a “significant impact” and another 31% saying they are having a “moderate impact.” Inflation and quality of labor are still the main two problems facing small business.

Finally, we saw inflationary expectations fall in the University of Michigan Consumer Sentiment Index. It was actually pretty dramatic, with next-year inflationary expectations falling from 4.2% to 3.3%. Longer-term inflationary expectations are still more or less stuck around 3%.