Weekly Tearsheet: Addressing housing affordability.

If mortgage rates fall, will housing become more affordable? I think for most people in the mortgage business, the answer is probably “yes.”

Housing affordability is a big topic these days, and the Dallas Fed put out an interesting study claiming that falling interest rates don’t necessarily lead to better housing affordability. The idea is that when mortgage rates fall, house prices generally rise. As any car salesman will tell you, people focus on the monthly payment, not the sticker price. Lower rates means a lower monthly payment, and people will bid up the price of properties, which offsets the benefit of lower mortgage rates.

Measuring housing affordability is a bit tricky, since there are a number of ways to look at the problem. The easiest way is to calculate an index based on house prices and incomes. The most common method is to divide the median house price by median income. This is an intuitive method of looking at the problem, but it has a major drawback - it ignores the impact that interest rates have on affordability. Since most people do take out a mortgage, the rate has a big impact on the monthly payment. A $400,000 house may be affordable at the median income when mortgage rates are 3% and not when rates are 7%.

Another measure of affordability looks at incomes, usually calculating the qualifying income (in other words, the income required to be able to afford a 20% down mortgage on the median house) divided by median income. This is a better approach to the affordability issue than using the ratio house price / income ratios, and it captures the effects of both prices and rates. You can see a chart of house prices to incomes below:

The Dallas Fed study suggests that falling mortgage will probably be met with rising home prices as it brings more potential home buyers back into the market. As they put it: “We emphasize that housing affordability not only depends on mortgage rates but also on house prices, which have competing effects. For example, when interest rates increase, house prices tend to decline. We present decompositions of housing affordability, showing the relative importance of the two competing effects matters, and lower interest rates do not necessarily improve housing affordability.”

This makes intuitive sense, and one of the issues I have with using qualifying income versus median income is that most people who aren’t in the mortgage business won’t understand the metric. I came up with an affordability method that I think does make intuitive sense.

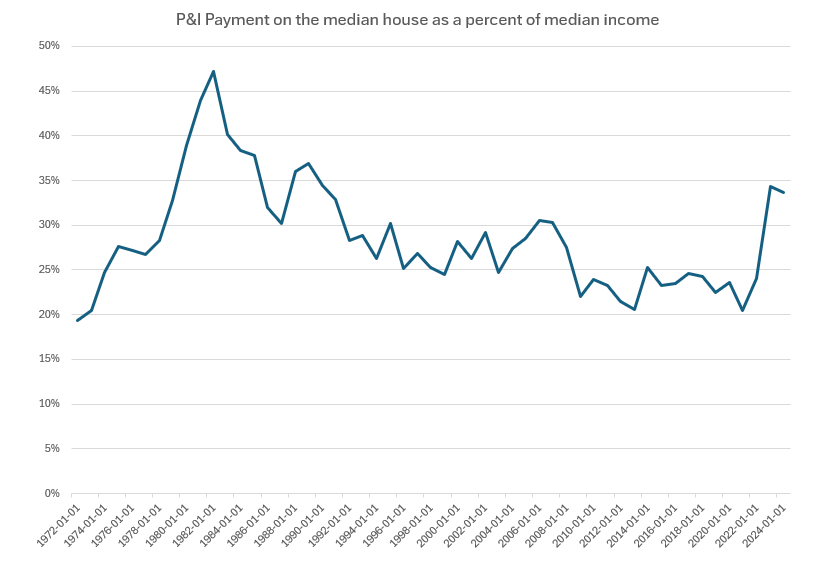

I plotted the expected principal and interest payment on the median home (prevailing mortgage rate with 20% down) and then divided it by median income. It gives you an idea of how much someone is spending on housing. When affordability is good, the P&I payment might take up 20% - 25% of the median income. At current levels, we are sitting at 34%. This might seem like a hopelessly unaffordable market, but it has been worse in the past. A lot worse.

In 1981, the P&I payment on the median house ate up 47% of median income. That was back when mortgage rates were 17%, and the first few years of a mortgage were 99% interest and almost zero principal.

Still, P&I payments are not the whole story - property taxes are going up, and homeowner’s insurance has been on a tear, rising 23% since 2023. Home maintenance costs are rising as well due to a shortage of skilled labor. Property taxes have risen about 4.1% overall, but some localities are seeing 30% increases in property taxes. One other important thing to take into account is income taxes. In the late 70s / early 80s, income taxes were higher, which made the interest deduction more valuable. In 1982, the top marginal tax rate was lowered from 70% to 50%, so the mortgage interest deduction was able to counteract the affordability issue at least somewhat.

Under this metric, housing affordability is at the worst levels since the 1980s when interest rates were much higher. So what pushed affordability levels back down? Not a drop in home prices: from 1981 to 1998 home prices rose about 4.1% per year. The improvement in affordability came from falling mortgage rates.

During the housing bubble, affordability again fell, which was driven more by rising house prices. In the aftermath of the housing bubble, we did see a big national decline in house prices.

I think the current situation resembles the 1980s more than 2008. For starters, home equity is at all-time highs, and the vast majority of mortgages are guaranteed by the US Government. I cannot envision a situation where we would have the forced selling that we did during the housing bust, where people with upside down mortgages were getting foreclosed on. Banks aren’t taking credit losses on their Fannie / Freddie mortgage backed securities. The situation now is one where there is sky-high demand, and interest rates have just embarked on a rapid rise. During inflationary periods, assets like real estate and commodities usually outperform, which happened in the 1970s.

There is an old saying in commodity markets: the cure for high prices is high prices. Homebuilding is answer to the affordability issue. While homebuilding has been lackluster in the aftermath of the real estate bubble, it used to be much higher. On a gross basis, housing starts are more or less where they were in the 1950s, when the population was much smaller. If you normalize housing starts by dividing by the number of households in the US, the chart looks like this:

We had a similar decline in homebuilding before the nadir of affordability in the early 1980s. I suspect we are going to (finally) see a renaissance in homebuilding, especially in cheaper exurbs since work-from-home has reduced the need to live close to the city and these exurbs have less byzantine permitting and regulatory processes. Note that we did see quite a homebuilding boom in the 1980s, which petered out as Gen X-ers became the primary first time homebuyer.

The experience of the 1980s provides a bit of a rejection of the Dallas Fed study. Home prices did rise on a nominal basis and were probably flat on an inflation-adjusted basis. Still, homebuilding and falling rates addressed the issue of affordability, and we might be in store for that going forward, with home prices rising at the rate of inflation and falling rates making the monthly payment cheaper. Hopefully we see a return of homebuilding, which will truly impact the affordability issue.