Weekly Tearsheet: The issue of shelter with inflation

The Spring Selling Season generally kicks off right around Super Bowl Sunday. The Spring Selling Season sets the tone for the upcoming year, especially for realtors, mortgage bankers, homebuilders, and many other professionals in the space. Since families generally prefer to move in the summer (for school reasons), the process kicks off in late winter.

Potential homebuyers are struggling with one of the least affordable housing markets ever as inflated home prices from the pandemic years collide with elevated mortgage rates. Given that the supply-demand imbalance is heavily skewed towards higher prices, homebuyers are left with hoping that interest rates fall. Falling mortgage rates are a lot less painful than falling home prices economically.

Unfortunately, we got some bad news on that front last week as the consumer price index surprised to the upside, sending the bond market into a tailspin. The 10 year bond was trading around 4.15% before the BLS reported that consumer prices rose 0.3% in January. Excluding food and energy, the index rose 0.4%, and that was enough to push bond yields above 4.3% at one point. Traders unwound March rate cut bets, leaving the Fed Funds futures handicapping a less-than-10% chance of a March cut.

Shelter accounted for about two thirds of the increase in the CPI, which presents a problem for the Fed. First of all, while home affordability is an important overall policy goal, managing the residential real estate market isn’t in the Fed’s job description. The Fed has the dual mandate of managing inflation in the context of full employment. Given that the job market is strong, and inflation is above the Fed’s target, they are pretty much forced to work on bringing down inflation. This means higher rates, which makes housing less affordable. This means that Fed policy is going to work against improving home affordability, not increasing it.

Brookings has a good piece on CPI and shelter, along with some of the drivers. Shelter inflation has been the last holdout, while inflation for other items is pretty much back to pre-pandemic levels:

The index for shelter is somewhat convoluted. It is based on a survey of 40,000 people, and it looks at rentals and owner-occupied housing. The cost of shelter for someone renting is the actual rent plus any government subsidies. For owner-occupied housing, it estimates what the homeowner would get if the property was rented out. This gets particularly difficult, especially since finding comparable rentals to single family housing can be difficult. This is a particularly acute issue at the high end of the spectrum - how does one calculate the approximate rental value of a 6,000 square foot house?

The Brookings study notes that rents as calculated under the inflation indices tend to lag market rents. Even though rental indices by companies like Zillow and CoreLogic have returned to pre-pandemic inflation rates, the CPI rental index has not.

As CPI and market rental indices converge, we should see the shelter portion of CPI return to normal, which will go a long way towards getting the Fed to its 2% target. The Fed is well aware of the shelter component’s impact, and there is a lot of multi-family supply headed to the market, particularly in the hottest markets in Florida, Texas and Arizona.

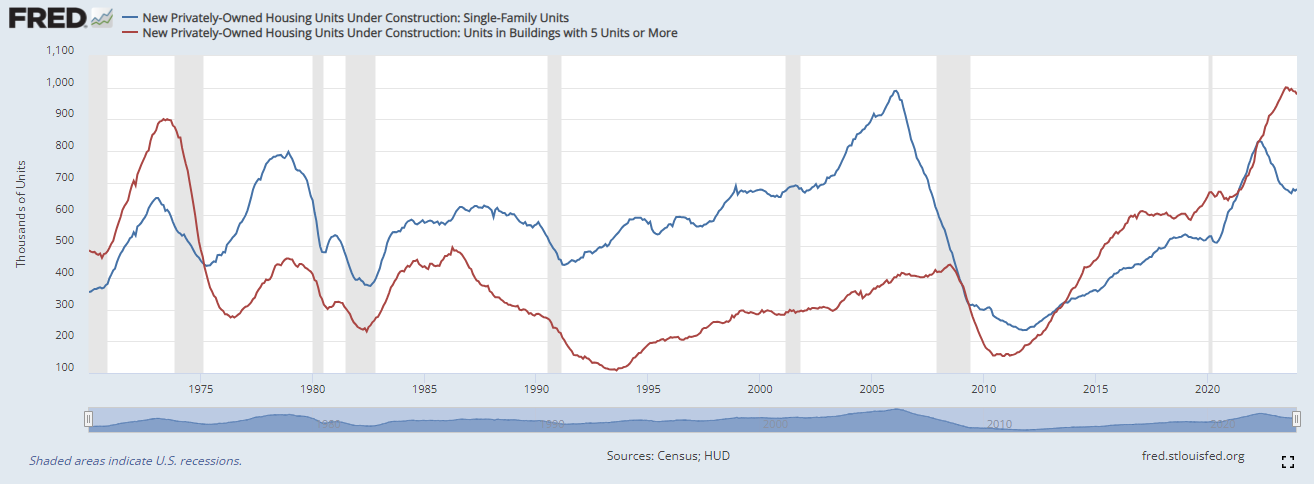

Housing starts were a disappointment, however winter housing starts numbers can often be affected by weather. That said, we have been seeing a trend where builders are shifting their focus from multi-family to single-family construction. Starts for 1 unit properties rose 22% on a year-over-year basis, while starts for 5 units fell 37% on a year-over-basis. Interestingly, in May of 2022, we saw a big drop in one-unit properties under construction while construction of 5+ unit properties accelerated.

We are seeing rental inflation cool in some of the hotter markets. Austin TX rents are actually down 3%, while Las Vegas and Miami are up a couple of percent. Note that some of these MSAs were up 20% - 30% during 2021 so rents are still expensive. They just aren’t increasing at unsustainable rates any more. Since a lot of this supply is in these markets, that should help push down rental inflation further.

Chicago Fed President Austan Goolsbee focused on the overall trend in inflation and acknowledged that the path to 2% inflation will not be a straight line. "Even if inflation comes in a bit higher for a few months...it would still be consistent with our path back to target. I don't support waiting until inflation on a 12-month basis has already achieved 2% to begin to cut rates." He did address somewhat the issue with CPI shelter indices, but at the moment it is something to watch.

We will get a first look at housing inventory for sale this week when the National Association of Realtors puts out its existing home sales report.